When we talk about affordability, we approach it from a simple equation:

Affordability = What You Earn – What You Pay for Housing

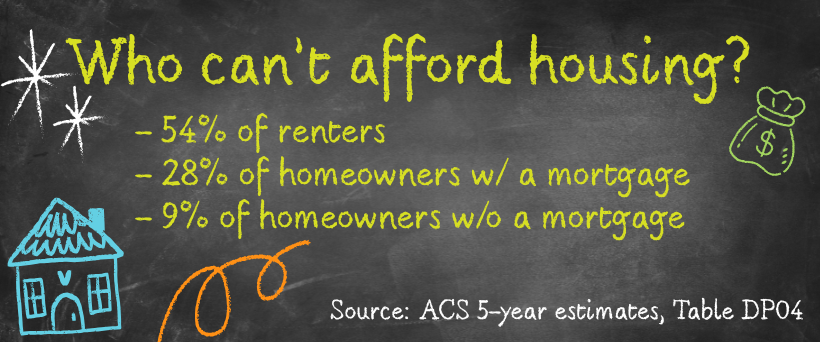

Ideally, you shouldn’t pay more than 30% of your gross income on housing. That’s not a number we made up; it’s the standard set by the federal government. This means you should be able to afford groceries, car payments, healthcare, and other bills with the remainder of your income. No matter if your household’s annual gross income is $40K or $400K, no more than 30% of that should go to your housing costs. When housing costs exceed 30%, households are considered cost-burdened, and if housing costs exceed 50%, households are considered extremely cost-burdened.

The unfortunate truth is that roughly 40% of Nashville residents cannot afford housing. According to the Living Wage Calculator, a family of four, comprised of two working adults and two children, needs to earn $25.62 an hour or $106,563 annually to afford to live in Nashville. Yet, the average family with kids makes just $72,430.

To fully understand the present-day affordability crisis, we have to understand the history that got us here. This issue will highlight the hard truths broken down into five eras. You’ll see that a series of government actions and market forces have made housing affordable for some, and unaffordable for others.

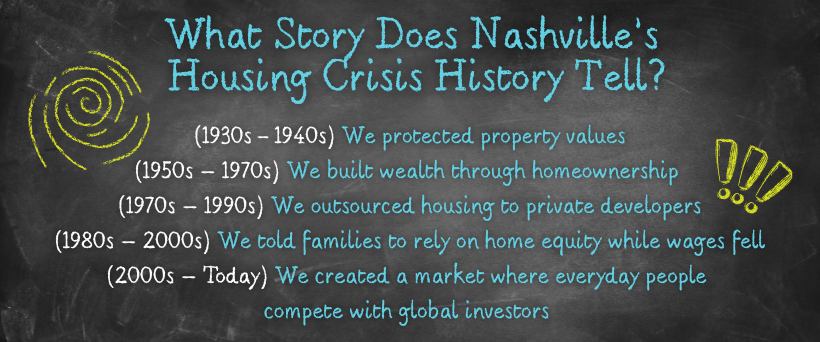

1. 1930s – 1940s | The Public Housing Era: Property Values Matter More Than People

During the Great Depression, the federal government intervened to “fix” the housing crisis. Programs led by the Home Owner’s Loan Corporation and the Federal Housing Association created mortgage markets and safe housing standards. Public housing was introduced as a solution to “slum conditions”—overcrowded, low-quality, urban housing for poor families. But as soon as landlords and realtors recognized that public housing would force them to raise their standards and compete on rental prices, they lobbied Nashville officials to limit its impact.

A Nashville Tennessean article from November 2, 1938, quoted Councilman Elkin Garfinkle’s comments that demonstrated private real-estate interests were threatened by public housing. He “…urged the council to ‘wait until the United States Housing Authority kicks the rich people out of the present slum clearance projects here… Let’s make the government show its good faith, before we give them a chance to set up more tax-free apartment houses to compete with our apartment houses in West End.’”

Advocates intended public housing to address real issues in the private market. In actuality, housing policy was used to further marginalize and exploit working-class, Black Nashvillians. The city’s elected officials and decision-makers used public housing to develop “buffer zones” between wealthy neighborhoods and poorer communities, and for downtown redevelopment.

Nashville was among the first cities to receive funding under the National Housing Act of 1949. However, rather than building housing, the city cleared 96 acres of substandard housing owned by slumlords for the Capitol Hill redevelopment and the James Robertson Parkway. Critics openly referred to this as “Negro removal” (Kreyling, 2016). This harmful legacy was only the start of the ongoing pattern we see today with landlords refusing to invest in the maintenance of their property, and when the time comes to redevelop the land, working-class Black renters are displaced from their homes.

First key moment: Housing policy was corrupted to preserve property values and landlord profits, not to guarantee decent housing for everyone.

2. 1940s – 1970s | The Homeownership State: When Housing Was Affordable

Homeownership was supercharged by federal policy after World War II because the GI Bill, FHA loans, and the 30‑year mortgage made buying a home affordable for millions of families, especially white families in newly built suburbs. Black families and families of color were systematically excluded from these opportunities until the Fair Housing Act of 1968 outlawed discriminatory housing practices.

This era cemented a new idea: Homeownership is the American Dream. And the government invested heavily to make it possible by subsidizing mortgages, funding highways, and supporting suburban growth. It also strengthened labor laws, ensuring wages grew with corporate profits. The theory was that working families needed a leg up to enter the middle class (Heathcott, 2012). Must’ve been nice for those who it worked for.

Second key moment: The government made homeownership affordable, but only for some.

3. 1970s – 1990s | The Market-Driven Turn: From Housing Provider to Real Estate Developer

By the 1970s, public housing was starved of funding by several presidential administrations, beginning with President Linden Johnson because of Vietnam War spending. Public housing became racially segregated and stigmatized as a place of crime, poverty, and government failure. The federal government opted to dismantle it, rather than repair the system its policymakers broke, using the following:

- Section 8 vouchers that moved families into private rental units.

- Low Income Housing Tax Credits handed responsibility for new “affordable” construction to private developers.

- HOPE VI, which demolished public housing in favor of mixed‑income, market‑driven projects with fewer affordable units.

These policy shifts pushed affordable housing providers, like the Metropolitan Development and Housing Agency, into the role of real estate developers. They produce housing that is less affordable, less stable, and more vulnerable to market pressures because of their dependence on tax incentives, deals, and debt.

Those actions marked the moment that the government gutted and abandoned public capacity to do things for its people. It unfairly exchanged public good for corporate welfare and privatization.

Third key moment: as housing policy embraced private real estate development, rental housing became less affordable for the working people it was meant to serve.

4. 1980s – 2000s | The Asset Building Era: Your Home Is Your Safety Net

While public housing was being dismantled, the government withdrew support from social programs that made life affordable for working people. Wages stagnated, jobs became less secure, and the global economy shifted. Instead of securing wages or strengthening worker protections, policymakers told families to rely on homeownership to build economic security.

Home equity became the fallback for retirement, education, healthcare, and emergencies. Meanwhile, families without homes and even those struggling to keep their homes were pushed into a cycle of debt. This marked a major turning point: homeowners now had a personal stake in keeping housing prices high and property taxes low—even if it made life unaffordable for everyone else.

It was in this context that “affordable housing” rose in policy debates—not because the government sought solutions, but because the shift to a market‑driven, homeownership‑centered model created predictable crises for people who were not homeowners.

Fourth key moment: Affordable housing became a crisis because homes were treated as investments first and places to live second, while the government’s framework that made economic mobility possible in earlier eras was steadily stripped away.

5. 2000s – Today | The Finance Era: You Compete With Investors

By the early 2000s, the U.S. had fully embraced a housing system built on homeownership and household debt. Federal policymakers aggressively pushed homeownership to the point that many working families were lured into predatory loans, prioritizing the housing boom over economic stability.

When the housing bubble burst in 2008, thousands of Tennesseans lost their homes—but for global finance, the crash soon created greater opportunity. Decades of financial deregulation had opened the door to pools of global capital searching for investments. Housing was the perfect target. Large investment firms, like American Homes 4 Rent, bought foreclosed properties in bulk, converting them into rental units and launching a new business model: housing as a financial asset. Rent payments became steady revenue streams, and housing portfolios were packaged and sold to investors for profit.

Likewise, existing apartment complexes have become increasingly bought out by private equity giants like Blackstone and Greystar. The sheer size of these corporate landlords allows them to raise rents faster, charge junk fees, and keep units off the market until prices climb. With the U.S. rental market more consolidated than ever into so few hands, collusion has become an issue. In 2024, the U.S. Department of Justice sued RealPage Inc. and six landlords, accusing them of using a price-fixing algorithm to work together and raise rents, which reportedly affected up to 30% of rental units and thousands of renters in Nashville.

All of this was supercharged during COVID. Remote workers drove home prices far beyond what local wages could support, and corporate landlords pushed rents to record highs. This is the culmination of decades of bad housing policy designed to favor private interests over working-class people. It has caused housing to shift from a basic need to a global investment vehicle. The history tells the story of a private market that will never meet people’s needs if left to itself. We need housing policies that prioritize the people’s need for safe homes, not investments.

Fifth key moment: Housing has morphed into a speculative financial asset, forcing everyday families to compete directly with billion-dollar corporate investors.

The result is a destructive cycle that:

- Drives wealth inequality by promoting home equity as the only safety net.

- Creates predictable housing crises by pitting homeowners against renters, and global capital against everyone.

That’s all for now, but next time we’ll get into how the destructive cycle leads to a rich city with a broke budget. Nashville is booming with development, but the city’s budget is busted.

Before you go, here’s information on two of our housing-related actions:

- Have you registered for The Housing Party? It’s our interactive, 90s-themed party featuring activities and games centered on all things housing, including ways to take action. Get your dance on with music from a live DJ, and enjoy good food. Rock your 90s attire or don’t—just be there!

🎉 The Housing Party – Monday, April 13, 2026, from 6-8 pm

📍 J.C. Napier Community Center, 73 Fairfield Ave, Nashville, TN 37210 - We’re calling local businesses to join the push for affordable housing solutions! Recently, Mayor Freddie O’Connell told Nashville residents that he wants them to be able to stay in the city. Of course, we loved the sentiment since it fits right into our “I Want You To Stay” pillar from last year’s budget season, and aligns with our continuous housing advocacy. But it’s going to take more than a verbal nod to ensure it becomes a reality.

Businesses need people, and people need affordable housing. From the owners themselves to their employees and customers, stable housing is crucial for everyone. If you agree, add your business name to our “We Want To Stay” letter to the mayor. It’s a unified statement urging him to secure support for housing solutions through budget funding. This will benefit the people who work every day to make a difference in Nashville, but are challenged by the rising cost of housing.